Changes to your ICBC insurance premiums

From September 1, 2019, we've made changes to the way insurance premiums are determined. Find out more about the changes and what to expect when you renew under this new model for the first time.

What's changing?

Changes to the renewal process: What to bring to your broker

We've moved to a more driver-based insurance model, and you'll be asked to list who drives your car. There are a few things you need to prepare and think about before you visit your broker to renew.

As of September 1, 2019, when you purchase or renew your insurance you will need:

- The driver's licence number and date of birth for each driver you want to list on your policy

- Of the listed drivers, who is the principal driver

- Your renewal reminder and insurance documents

- A photo of your current odometer reading if your car is driven less than 5,000 km in a year (a potential discount may apply at your next renewal)

- To check your ownership manual, or with your dealership, to see if your vehicle has factory-installed autonomous emergency braking (AEB). Vehicles equipped with AEB will be eligible for a discount.

Why do you need to know who drives my car?

You'll be asked to list those who drive your car such as household members, employees, learners and others who use your car. If one of the listed drivers causes a crash in your car, the at-fault driver will be held accountable for the crash.

You can add or remove drivers any time and it doesn’t cost anything. Adding drivers won’t necessarily change your premium – it will depend on many factors including the driving experience and crash history of all the listed drivers.

What is "the principal driver"?

You'll be asked to declare the principal driver – the person who drives the car the most. The majority of the premium (75%) will be based on the principal driver.

Why do you want to know how much my car is driven in a year?

A new discount is available for vehicles that are driven less than 5,000 km in a year.

If you think you may qualify for this discount, your broker can record your odometer reading. At your next policy renewal, if the mileage is less than 5,000 km, a 10 per cent discount will apply to your insurance. More information is available on the Discounts and savings page.

Why is there a discount for autonomous emergency braking?

Vehicles equipped with factory-installed autonomous emergency braking (AEB) will be eligible for a 10 per cent discount as AEB has been statistically shown to help prevent crashes. More information is available on the Discounts and savings page.

The way we set insurance premiums

Driving experience and crash history now play a bigger role in determining premiums. Other factors, like where you live and how you use your car, have also been updated.

Experience and crash history affect what you pay

The first part of your Basic insurance premium looks at driving experience and crash history.

These two factors already affected your premium, but as of September 1, 2019, they have a greater impact. In general, the more crashes you cause, the more you will pay in insurance. The more years of driving experience you accumulate, the more discounts you’ll earn.

We will also ask that you list who drives your car so they can be noted on your policy. Household members, employees and regular drivers should be listed if they're going to use your car. If a learner will be driving your car, a new additional premium will also apply.

This is the area that is changing the most for B.C. drivers – find out all the details below or watch our video to learn more.

Why do I need to list other drivers?

Under the old model, at-fault crashes followed the vehicle owner, rather than the driver. For example, if your friend borrowed your vehicle and caused a crash, the claim applied to your record, not theirs, even though you didn't cause the crash.

Under the new model, at-fault crashes follow the driver, not the vehicle owner. So if your friend causes a crash using your vehicle, the claim is counted on their driving record, not yours.

Listing those who drive your car helps to make sure the right person is held accountable for the crash, and the risk involved in insuring your car is more accurately assessed.

Watch our video to find out more about how to list drivers.

How do the listed drivers impact my premium?

The majority (75%) of your Basic insurance premium is based on the principal driver (the person who will drive the vehicle the most). Of the other listed drivers, the one with the highest level of risk will make up the remaining 25%.

However, if the listed driver is lower-risk than the principal driver, there will only be a reduction in the premium if that listed driver is a household member or employee. This helps prevent people from adding lower-risk drivers to their policies simply to artificially reduce their premiums. Adding drivers won't necessarily increase your premium. It depends on various factors, such as each listed driver's experience and crash history.

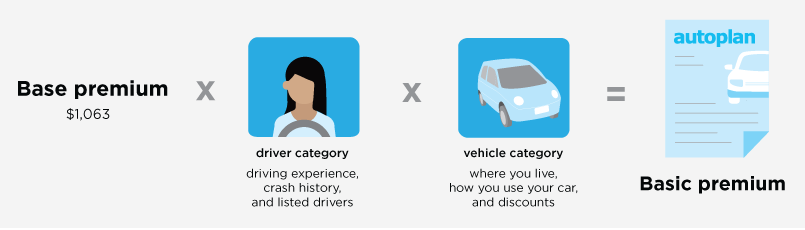

How are my premiums calculated?

Each insurance policy starts with a base premium. (The base premium for Basic insurance as of April 1, 2019, is $1,063). The premium then increases or decreases depending on each individual’s factors that fall under the driver and vehicle categories.

Explore the Interactive insurance education tool

Our interactive tool uses driver types to walk you though the new insurance model and give you a general idea of how adding drivers may impact your premiums.

Get an estimate online

If you’ve received your renewal reminder in the mail (44 days before your policy expires) then you’re ready to pre-list drivers and get an estimate online based on your current coverages. If you’re outside of your insurance renewal window, use the interactive education tool instead.

What if I want to be able to lend my car to anyone?

If you would like the flexibility to be able to lend your car occasionally to a driver not listed on your policy, Unlisted Driver Protection can provide peace of mind. It protects you from a potential one-time financial consequence should an occasional driver, not listed on your policy, cause a crash using your car. Find out more about the potential Unlisted Driver Accident Premium.

Unlisted Driver Protection will not protect you from this financial consequence, though, if any of these people cause a crash in your car, as they should be listed on your policy:

- Household members

- Employees

- Anyone who has driven any of your vehicles for more than 12 days in the last 12 months before the crash

Anyone who has caused a crash in any of your vehicles in the last five years (from September 1, 2019) and unlicensed drivers are also excluded from this protection.

Unlisted Driver Protection is available at no cost to you unless an unlisted driver causes a crash using your car. After the first unlisted driver crash occurs, you will need to pay for this protection, if you wish to have it, at your next renewal. If unlisted drivers continue to crash your car, the cost of this protection will increase.

What if an unlisted driver causes a crash in my car?

You may face a one-time financial consequence if you don’t have Unlisted Driver Protection or if it doesn’t apply (for example, if the unlisted driver is a household member, employee or other regular driver that should have been listed).

This financial consequence will depend on a number of factors, such as their driving experience and crash history. We will look at how much your Basic and Optional premiums would have been, had you listed that driver who caused the crash.

If there is no difference in the premium, there wouldn’t be a penalty to pay. If there is a difference, the financial consequence would be 15 times that amount. Find out more about the Unlisted Driver Accident Premium.

There will be exemptions for extraordinary situations, such as when an unlisted driver uses your vehicle for a medical emergency. Mechanics and valets who may drive your car are covered by their own policy.

Although the Unlisted Driver Protection is initially free, if an unlisted driver causes a crash in your car, you’ll need to pay for this protection. If more unlisted driver crashes occur, the cost of this protection will continue to increase.

Have you introduced crash forgiveness?

Yes, we know that crashes do happen so we will forgive one crash after 20 years of driving experience, provided you have been crash-free for the last 10.

Can I still repay a claim to protect my premium?

Previously, if you were found responsible

(at fault) for a crash that didn't involve costly vehicle damage, you could

repay the cost of the claim to ICBC so it wouldn’t affect your insurance

premium. However, this meant that the true risk of drivers repaying claims

wasn’t accurately represented.

So, for crashes on or after September 1,

2019, claim repayment is only possible if the claim amount is $2,000 or

less.

How is driving experience recognized?

Generally, drivers with more years of driving experience and no at-fault crashes will see greater discounts. You will be able to receive Basic insurance discounts for up to 40 years of driving experience, up from nine years of crash-free driving.

As for inexperienced drivers, previously their Basic insurance premiums were significantly discounted. We will continue to offer them discounted premiums, however, these discounts will be reduced if they cause a crash, and eliminated if they cause a second one within the five-year scan period.

How are you recognizing driving experience of new B.C. residents?

New B.C. residents already received driving experience credit upon starting to drive in B.C. That credit has been increased from a maximum of eight years to a maximum of 15. However, their premiums reflect the additional risk they pose during their first three years driving in B.C.

New residents will no longer be asked to provide previous insurance documentation. However, new residents who get their B.C. driver’s licence after September 1, 2019 need to prove their driver’s licence history to be eligible for up to 15 years of driving experience credit.

Should I list learner drivers? How does that impact my premium?

Yes, if a learner driver will be using your car, you should list them and a new additional premium will apply. The learner premium recognizes the risk that a learner driver represents and helps cover the costs of crashes caused by learners. The learner premium ranges from $130 to $230 per year, depending on where you live. You don't need to pay the premium for each learner – it is one cost to cover all learners using your car.

For learner drivers, time spent in the learner stage does not count towards their driving experience, and crashes caused by learners will not go on their driving record either. We don't want to penalize learners if they were to cause a crash while they are learning to drive.

Have you changed the seniors' or disability discounts?

There are no changes to the current discount for qualifying persons with disabilities.

Seniors continue to receive a Basic insurance discount and now benefit from more years of driving experience being considered – up to 40 years from the current nine years of crash-free driving. However, their discount will be reduced if they cause a crash and eliminated if they cause a second crash within the ten-year scan period.

Have you changed the way premiums are set for Optional insurance coverages?

Yes, we introduced changes to make premiums for Optional coverages align with the changes made to the Basic rate model to make sure drivers are held more accountable for their driving decisions.

As of September 1, 2019, frequent or serious driving convictions resulting from driving violations that occurred on or after June 10, 2019 have the potential to impact your premiums for both Collision and Extended Third Party Liability coverages.

- Two or more convictions for minor offences (such as failure to stop at a stop sign or speeding) or one serious offence (use of an electronic device while driving, impaired driving or excessive speeding) within a three-year period, will result in an increase in premiums for these coverages.

- Those premiums will increase with the frequency and seriousness of the convictions. ICBC will ultimately scan back over a three-year period for driving convictions by June 10, 2022.

- The goal is to benefit lower-risk drivers – those who don’t cause crashes or get driving convictions.

- For more information, read the news release and factsheet.

What's a driver factor?

Every driver in B.C. has a driver factor – a 3 decimal number that represents your driving experience and crash history. The driver factor also takes into consideration whether you're a senior or a new resident. The driver factor baseline is 1.000 with a lower number being more favourable. As you gain driving experience, and for each year that you remain crash-free, your driver factor will improve.

How will my insurance be affected if I cause a crash in an employer's vehicle?

If you cause a crash while driving a fleet vehicle, your non-fleet insurance premiums will not be impacted. For more information visit Drivers of fleet or business vehicles.

Where you live and how you use your car

The next part that determines your Basic insurance premium looks at where you live (in insurance terms, this is your territory) and how you use your car (your rate class).

Both territory and rate class help to determine your premiums. We’ve updated our data to recognize the changes in communities and vehicle use across B.C.

How do the territory and rate class changes affect my premium?

Some customers will see this portion of their premium from territory and rate class either increase or decrease – it all depends on their individual situation. Where you live is only one factor used to calculate your Basic premium. So even if there is an increase to your territory or rate class, you could still see an overall decrease based on the other factors such as driver experience and crash history.

New discounts

We have also introduced two new vehicle-related discounts:

- Vehicles with original, manufacturer-installed autonomous emergency braking are recognized with a 10 per cent discount.

- Vehicles that are driven less than 5,000 km in a year are eligible for a 10 per cent discount.

How do I get the low-kilometre discount?

If you think you qualify for the low-kilometre discount, bring a current odometer reading to your broker when you next renew your insurance. More information is available on the Discounts and savings page.

What is autonomous emergency braking?

Autonomous emergency braking (AEB) is a safety feature that uses technology to anticipate when a vehicle is about to have a front-end collision and automatically engages the brakes without the driver’s action.

If you’re not sure whether your vehicle has AEB, check with your dealership or look in your ownership manual.

Wondering how much your insurance will be this year?

If you've received your renewal reminder, you can get an estimate of your premiums now. Or, try our interactive tool to learn how listing drivers can impact your premiums.

Pre-list drivers and get an estimate

If you've received your renewal reminder, you can log in to our tool and pre-list your drivers now to estimate how much your insurance will cost.

Learn more about listing drivers

If you’re not due to renew soon but want to learn how listing drivers will impact your premiums, you can use our interactive tool to learn more about the changes.